Beautiful Bad Debts Recovered In Trial Balance Notes Receivable On Sheet

What Are Bad Debts Example Journal Entry Accountingcapital

Some times it so occurs that the bad debts formerly written off are consequently recovered. 8000 Outstanding Rent Rs. Bad Debts AC Dr. An entity may not be able to recover its balances outstanding in respect of certain receivables. His debt is declared bad then the amount needs to be written off deducted from the Debtors or sales ledger. When the debts that were written off in the past years is now recovered either fully or partly is termed as bad debt recovery. This is recorded as bad debt recovery. Find your perfect Bad Debts Recovered In Trial Balance for your desktop and mobile devices. Profit and Loss Ac Profit Rs. Prepare trial balance from the following information prepaid expense rs5 000 profit and loss a c profit rs8 000 outstanding rent rs2 000 bad debts rec.

As you can see the entry above actually does not affect the debtors control account at all you dont have to show that more is owing to us now.

As you can see 10000 1000000 001 is determined to be the bad debt expense that management estimates to incur. This may be clearer than crediting the recovery to the bad debts expense account because that would obscure the expense from bad debts. Bad Debts recorded in Trial Balance is not recorded in balance sheet as adjustments have already been made. Where do you think the other side of the entry is going when you create a provision for bad debts. 1000 Due to Mohan Rs. Find your perfect Bad Debts Recovered In Trial Balance for your desktop and mobile devices.

This may be clearer than crediting the recovery to the bad debts expense account because that would obscure the expense from bad debts. In order to account for the bad debt recovery it is first necessary to reinstate the accounts receivable balance for the amount received. Bad Debts Recovery. Bad debts could arise for a number of reasons such as. As you can see 10000 1000000 001 is determined to be the bad debt expense that management estimates to incur. An entity may not be able to recover its balances outstanding in respect of certain receivables. Sometimes bad debts may occur at the end of accounting period after the accounts are balanced and the trial balance is prepared. Under the percentage of receivables method of estimating bad debt expense companies prepare an aging schedule as shown below. Just as some of the expenses of the trading period may not be actually paid until after the close of the trading period some other expenses may be paid in advance so much. Some times business receives a pleasant surprise when it recovers the bad debts which were previously written off as bad debts.

At times a debtor whose account had earlier been written off by a creditor as a bad debt may decide to make a payment this is called the recovery of bad debts. We have passed the following entries. 1000 Due to Mohan Rs. Bad Debts AC Dr. The accounting records will show the following bookkeeping entries for the bad debt recovery. Again the percentages are determined by past experience and past data. Similar to writing off accounts receivable the recovery of bad debt affects only the balance sheet accounts. In such case the cash account is debited and bad debts recovered account is credited because the amount so received is an increase in the business. Profit and Loss Ac Profit Rs. Suppose in the case of premises sublet rent for the month of March has not yet been received.

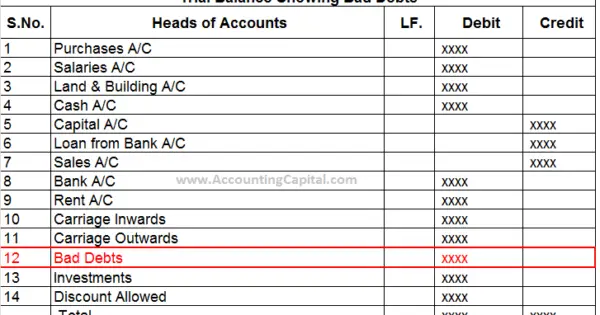

We have passed the following entries. Sometimes bad debts may occur at the end of accounting period after the accounts are balanced and the trial balance is prepared. Profit and Loss Ac Profit Rs. Cr Bad Debts Recovered income. Now this Bad Debts appears in the Trial Balance will feature in the Debit side of the Profit and Loss Account as it is a loss of the business. One must then pass the following entry accounts being prepared up to 31st March. Under the percentage of receivables method of estimating bad debt expense companies prepare an aging schedule as shown below. This may be clearer than crediting the recovery to the bad debts expense account because that would obscure the expense from bad debts. Bad Debts AC Dr. In such a case bad debts should be brought into account by passing the adjusting entry that is debiting bad debts account and crediting sundry debtors account.

2000 received from Smith whose account was previously written off as bad debt should be credited to a Bad debts recovered Account b Smiths Account c Cash Account d None of the options. Sometimes bad debts may occur at the end of accounting period after the accounts are balanced and the trial balance is prepared. The credit balance on the account is then transferred to the credit of the statement of profit or loss added to gross profit or included as a negative in the list of expenses. This may be clearer than crediting the recovery to the bad debts expense account because that would obscure the expense from bad debts. Just as some of the expenses of the trading period may not be actually paid until after the close of the trading period some other expenses may be paid in advance so much. Suppose in the case of premises sublet rent for the month of March has not yet been received. An entity may not be able to recover its balances outstanding in respect of certain receivables. Now this Bad Debts appears in the Trial Balance will feature in the Debit side of the Profit and Loss Account as it is a loss of the business. Some times it so occurs that the bad debts formerly written off are consequently recovered. In such a case bad debts should be brought into account by passing the adjusting entry that is debiting bad debts account and crediting sundry debtors account.

An entity may not be able to recover its balances outstanding in respect of certain receivables. Some times business receives a pleasant surprise when it recovers the bad debts which were previously written off as bad debts. Bad debts could arise for a number of reasons such as. 8000 Outstanding Rent Rs. It is usually an income and hence. 5000 Bank overdraft Rs. Similar to writing off accounts receivable the recovery of bad debt affects only the balance sheet accounts. Sometimes bad debts may occur at the end of accounting period after the accounts are balanced and the trial balance is prepared. 2000 Bad Debts Recovered Rs. DR Bad Debts Expense Income Statement CR Provision for Bad Debts Balance Sheet contra account to Accounts Receivable.