Breathtaking Expected Credit Loss Double Entry Understanding P&l Reports

Adjustments To Financial Statements Students Acca Global Acca Global

They are the weighted average credit losses with the probability of default as the weightBecause ECLs also factor in the timing of payments a credit loss or. An expected credit loss ECL is the expected impairment of a loan lease or other financial asset based on changes in its expected credit loss either over a 12-month period or its lifetime. The concept of expected credit losses ECLs means that companies are required to look at how current and future economic conditions impact the amount of loss. When changes in expected cash flows are in line with original contractual terms but they do not result from movements in market interest rates an entity recalculates the amortised cost using financial instruments original effective interest rate EIR. Credit losses are not just an issue for banks. ECLs on trade receivables are measured by applying either the general model or. On top of the ECLs specific allowances will continue to be recognised if certain loss events have occurred as was the case under IAS 39. For example the specific adjusted loss rate should be applied to the balance of each age-band for the receivables in each group. In order to adjust this balance a. They are expected losses from delinquent and bad debt or other credit.

Loss rate Expected credit loss.

Cash flows are discounted by using the original effective interest rate of the financial instrument. The amount of change in fair value attributable to changes in credit risk of the liability presented in OCI and the remaining amount presented in PL. They are the weighted average credit losses with the probability of default as the weightBecause ECLs also factor in the timing of payments a credit loss or. Expected Credit Loss ECL model Credit loss is the difference between the present value of contractual cash flows and the present value of expected cash flows associated with a financial asset. An expected credit loss ECL is the expected impairment of a loan lease or other financial asset based on changes in its expected credit loss either over a 12-month period or its lifetime. The provision for credit losses is treated as an expense on the companys financial statements.

12-month ECL are the expected credit losses that result from default events. As a result a one-off gain or loss is recognised in PL IFRS 9B546. The new guidance allows the recognition of the full amount of change in the fair value in profit or loss only if the presentation of changes in the liabilitys credit risk in other comprehensive income would create or enlarge an. Under this standard an entity recognizes its estimate of lifetime expected credit losses as an allowance which the FASB believes will result in more timely recognition of such losses. Lifetime ECLs are an expected present valuemeasure of losses that arise if a borrower defaults on its obligation throughout the life of the loan. An expected credit loss ECL is the expected impairment of a loan lease or other financial asset based on changes in its expected credit loss either over a 12-month period or its lifetime. In order to adjust this balance a. They are the weighted average credit losses with the probability of default as the weightBecause ECLs also factor in the timing of payments a credit loss or. Cash flows are discounted by using the original effective interest rate of the financial instrument. It is the expected credit loss resulting from default events on a financial instrument that are possible within 12 months after the reporting date.

They are expected losses from delinquent and bad debt or other credit. An expected credit loss ECL is the expected impairment of a loan lease or other financial asset based on changes in its expected credit loss either over a 12-month period or its lifetime. Within maturity 0-30 days 800. ECLs on trade receivables are measured by applying either the general model or. For example the specific adjusted loss rate should be applied to the balance of each age-band for the receivables in each group. 12-month ECL are the expected credit losses that result from default events. They are the weighted average credit losses with the probability of default as the weightBecause ECLs also factor in the timing of payments a credit loss or. Credit losses are not just an issue for banks. Cash flows are discounted by using the original effective interest rate of the financial instrument. Expected Credit Loss ECL model Credit loss is the difference between the present value of contractual cash flows and the present value of expected cash flows associated with a financial asset.

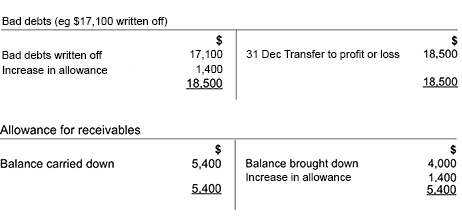

After this journal entry is recorded Gems July 31 balance sheet will report the net realizable value of its accounts receivables at 220000 230000 debit balance in Accounts Receivable minus the 10000 credit balance in Allowance for Doubtful Accounts. Within maturity 0-30 days 800. Credit losses are not just an issue for banks. For example the specific adjusted loss rate should be applied to the balance of each age-band for the receivables in each group. Lifetime ECLs are an expected present valuemeasure of losses that arise if a borrower defaults on its obligation throughout the life of the loan. The new standard is also intended to reduce the complexity of US GAAP by decreasing the number of credit loss models that entities can use to account for debt instruments. Loss rate Expected credit loss. Cash flows are discounted by using the original effective interest rate of the financial instrument. The expected credit losses are recorded in profit or loss on initial recognition in an allowance account for the respective item in the statement of financial position and updated at every reporting date. It estimates 10 of its accounts receivable will be uncollected and proceeds to create a credit entry of 10 x 40000 4000 in allowance for credit losses.

ECLs on trade receivables are measured by applying either the general model or. An expected credit loss ECL is the expected impairment of a loan lease or other financial asset based on changes in its expected credit loss either over a 12-month period or its lifetime. 347 360 days. The expected credit loss of each sub-group determined in Step 1 should be calculated by multiplying the current gross receivable balance by the loss rate. The new guidance allows the recognition of the full amount of change in the fair value in profit or loss only if the presentation of changes in the liabilitys credit risk in other comprehensive income would create or enlarge an. In order to adjust this balance a. The new standard is also intended to reduce the complexity of US GAAP by decreasing the number of credit loss models that entities can use to account for debt instruments. The amount of change in fair value attributable to changes in credit risk of the liability presented in OCI and the remaining amount presented in PL. Loss rate Expected credit loss. It estimates 10 of its accounts receivable will be uncollected and proceeds to create a credit entry of 10 x 40000 4000 in allowance for credit losses.

Lifetime ECLs are an expected present valuemeasure of losses that arise if a borrower defaults on its obligation throughout the life of the loan. When changes in expected cash flows are in line with original contractual terms but they do not result from movements in market interest rates an entity recalculates the amortised cost using financial instruments original effective interest rate EIR. Assets 12-month expected credit losses ECL are recognised and interest revenue is calculated on the gross carrying amount of the asset that is without deduction for credit allowance. 347 360 days. The concept of expected credit losses ECLs means that companies are required to look at how current and future economic conditions impact the amount of loss. They are expected losses from delinquent and bad debt or other credit. The expected credit loss of each sub-group determined in Step 1 should be calculated by multiplying the current gross receivable balance by the loss rate. In this case the interest revenue is recognized based on effective interest rate method on gross carrying amount so no loss allowance is taken into account. As a result a one-off gain or loss is recognised in PL IFRS 9B546. It is the expected credit loss resulting from default events on a financial instrument that are possible within 12 months after the reporting date.