Nice Isa Audit Opinion Accounts Receivable Cash Flow Statement

Revised Auditor Report Isa 700 Isa 705 Isa 706 And Isa 720

As required by the standard auditors will have to issue the opinion on the clients financial statements whether those financial statements after audited are prepared in all material respected and compliance with the framework that they used or not. This ISA has been revised to conform to the enhanced auditor reporting requirements in ISA 700 Revised Forming an Opinion and Reporting on Financial Statements. 6 Paragraphs 3536 deal with the phrases used to express this opinion in the case of a fair presentation. Of the International Auditing and Assurance Standards Board IAASB. An auditors opinion is a certification that accompanies financial statements. 5 ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing paragraph 13a. This revised ISA deals with the auditors responsibility to form an opinion on the financial statements as well as the form and content of the auditors report issued as a result of an audit of financial statements. Extant ISA 510 restricts the circumstances when the auditor can express an unmodified opinion on the closing financial position of the entity and a qualified opinion or disclaimer of opinion on the results of operations and cash flows split opinion to jurisdictions permitting it. This Auditing Standard conforms with International Standard on Auditing ISA 700 Forming an Opinion and Reporting on a Financial Report issued by the International Auditing and Assurance Standards Board IAASB an independent standard-setting board of the International Federation of. International Standard on Auditing ISA 705Revised Modifications to the Opinion in the Independent Auditors Report.

International Standard on Auditing ISA 705 Revised Modifications to the Opinion in the Independent Auditors Report should be read in conjunction with ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing.

Application of ISA 701 when a Qualified or Adverse Opinion is issued. Extant ISA 510 restricts the circumstances when the auditor can express an unmodified opinion on the closing financial position of the entity and a qualified opinion or disclaimer of opinion on the results of operations and cash flows split opinion to jurisdictions permitting it. Changes to this ISA relate primarily to how the form and content of the auditors report is affected when the auditor expresses a modified opinion. International Standard on Auditing ISA 705 Revised Modifications to the Opinion in the Independent Auditors Report should be read in conjunction with ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. International Standard on Auditing ISA 705Revised Modifications to the Opinion in the Independent Auditors Report. ISA 705 Revised Modifications to the Opinion in the Independent Auditors Report outlines the requirements when the auditor concludes that the audit opinion should be modifiedISA 705 Revised requires that the auditor includes a Basis for QualifiedAdverse Opinion section in the auditors report.

Of the International Auditing and Assurance Standards Board IAASB. International Standard on Auditing ISA 705 Revised Modifications to the Opinion in the Independent Auditors Report should be read in conjunction with ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. This revised ISA deals with the auditors responsibility to form an opinion on the financial statements as well as the form and content of the auditors report issued as a result of an audit of financial statements. As required by the standard auditors will have to issue the opinion on the clients financial statements whether those financial statements after audited are prepared in all material respected and compliance with the framework that they used or not. This ISA has been revised to conform to the enhanced auditor reporting requirements in ISA 700 Revised Forming an Opinion and Reporting on Financial Statements. 6 Paragraphs 3536 deal with the phrases used to express this opinion in the case of a fair presentation. It is based on an audit of the procedures and records used to produce the statements and delivers an opinion as to. International Standard on Auditing ISA 705 Modifications to the Opinion in the Independent Auditors Report should be read in conjunction with ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. International Standard on Auditing ISA 700 Revised Forming an Opinion and Reporting on Financial Statements should be read in conjunction with ISA 200 Overall Objectives of theIndependent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. Extant ISA 510 restricts the circumstances when the auditor can express an unmodified opinion on the closing financial position of the entity and a qualified opinion or disclaimer of opinion on the results of operations and cash flows split opinion to jurisdictions permitting it.

This ISA has been revised to conform to the enhanced auditor reporting requirements in ISA 700 Revised Forming an Opinion and Reporting on Financial Statements. International Standard on Auditing ISA 700 Revised Forming an Opinion and Reporting on Financial Statements should be read in conjunction with ISA 200 Overall Objectives of theIndependent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. This ISA applies to an audit of a complete set of general purpose financial statements. 5 ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing paragraph 13a. Application of ISA 701 when a Qualified or Adverse Opinion is issued. In order to form an opinion auditor must adhere to the requirements of ISA 700 and under the circumstances of engagement appropriate select the type of opinion to be expressed ie. If you have questions about ASAISA 700 add them in the comments belowFind ASA 700 here httpwwwauasbgovauPronouncementsAustralian-Auditing-Standard. This Auditing Standard conforms with International Standard on Auditing ISA 700 Forming an Opinion and Reporting on a Financial Report issued by the International Auditing and Assurance Standards Board IAASB an independent standard-setting board of the International Federation of. ISA 705 Revised Modifications to the Opinion in the Independent Auditors Report outlines the requirements when the auditor concludes that the audit opinion should be modifiedISA 705 Revised requires that the auditor includes a Basis for QualifiedAdverse Opinion section in the auditors report. Qualified adverse or disclaimer of opinion.

Changes to this ISA relate primarily to how the form and content of the auditors report is affected when the auditor expresses a modified opinion. ISA 700 Revised is effective for audits of financial statements for periods ending on. This revised ISA deals with the auditors responsibility to form an opinion on the financial statements as well as the form and content of the auditors report issued as a result of an audit of financial statements. ISA 705 Revised Modifications to the Opinion in the Independent Auditors Report outlines the requirements when the auditor concludes that the audit opinion should be modifiedISA 705 Revised requires that the auditor includes a Basis for QualifiedAdverse Opinion section in the auditors report. International Standard on Auditing ISA 700 Revised Forming an Opinion and Reporting on Financial Statements should be read in conjunction with ISA 200 Overall Objectives of theIndependent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. An auditors opinion is a certification that accompanies financial statements. Extant ISA 510 restricts the circumstances when the auditor can express an unmodified opinion on the closing financial position of the entity and a qualified opinion or disclaimer of opinion on the results of operations and cash flows split opinion to jurisdictions permitting it. We would like to draw attention to the footnotes in the illustrations of the Appendix which highlight to the auditors that when the audit opinions on the financial statements are modified there may be implications on the audit opinion on the accounting and other records as well which the auditors would need to assess and evaluate on a case-by-case basis. 5 ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing paragraph 13a. International Standard on Auditing ISA 705Revised Modifications to the Opinion in the Independent Auditors Report.

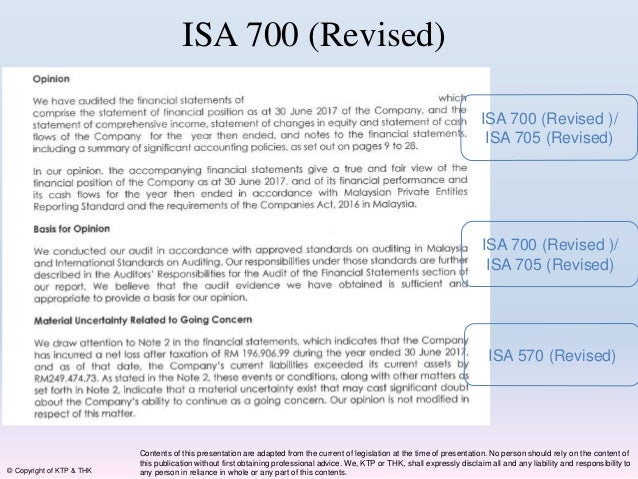

Application of ISA 701 when a Qualified or Adverse Opinion is issued. ISA 700 Revised is effective for audits of financial statements for periods ending on. We would like to draw attention to the footnotes in the illustrations of the Appendix which highlight to the auditors that when the audit opinions on the financial statements are modified there may be implications on the audit opinion on the accounting and other records as well which the auditors would need to assess and evaluate on a case-by-case basis. ISA 570 REVISED GOING CONCERN International Standard on Auditing ISA 570 Revised Going Concern should be read in conjunction with ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. International Standard on Auditing ISA 705Revised Modifications to the Opinion in the Independent Auditors Report. An auditors opinion is a certification that accompanies financial statements. When the auditor modifies the audit opinion the auditor shall use the heading Qualified Opinion. This ISA has been revised to conform to the enhanced auditor reporting requirements in ISA 700 Revised Forming an Opinion and Reporting on Financial Statements. This revised ISA deals with the auditors responsibility to form an opinion on the financial statements as well as the form and content of the auditors report issued as a result of an audit of financial statements. International Standard on Auditing ISA 700 Revised Forming an Opinion and Reporting on Financial Statements should be read in conjunction with ISA 200 Overall Objectives of theIndependent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing.

This Auditing Standard conforms with International Standard on Auditing ISA 700 Forming an Opinion and Reporting on a Financial Report issued by the International Auditing and Assurance Standards Board IAASB an independent standard-setting board of the International Federation of. Changes to this ISA relate primarily to how the form and content of the auditors report is affected when the auditor expresses a modified opinion. It is based on an audit of the procedures and records used to produce the statements and delivers an opinion as to. ISA 700 is used to form unmodified audit opinion and ISA 705 is the guidance that should use by the auditor to issue a modified opinion. Qualified adverse or disclaimer of opinion. In order to form an opinion auditor must adhere to the requirements of ISA 700 and under the circumstances of engagement appropriate select the type of opinion to be expressed ie. ISA 700 Revised is effective for audits of financial statements for periods ending on. ISA 705 Revised is effective for audits of financial statements for periods. International Standard on Auditing ISA 700 Revised Forming an Opinion and Reporting on Financial Statements should be read in conjunction with ISA 200 Overall Objectives of theIndependent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. An auditors opinion is a certification that accompanies financial statements.