Ace Prepare Financial Reports Deferred Tax Liability Calculation Example Uses Of Trial Balance In Accounting

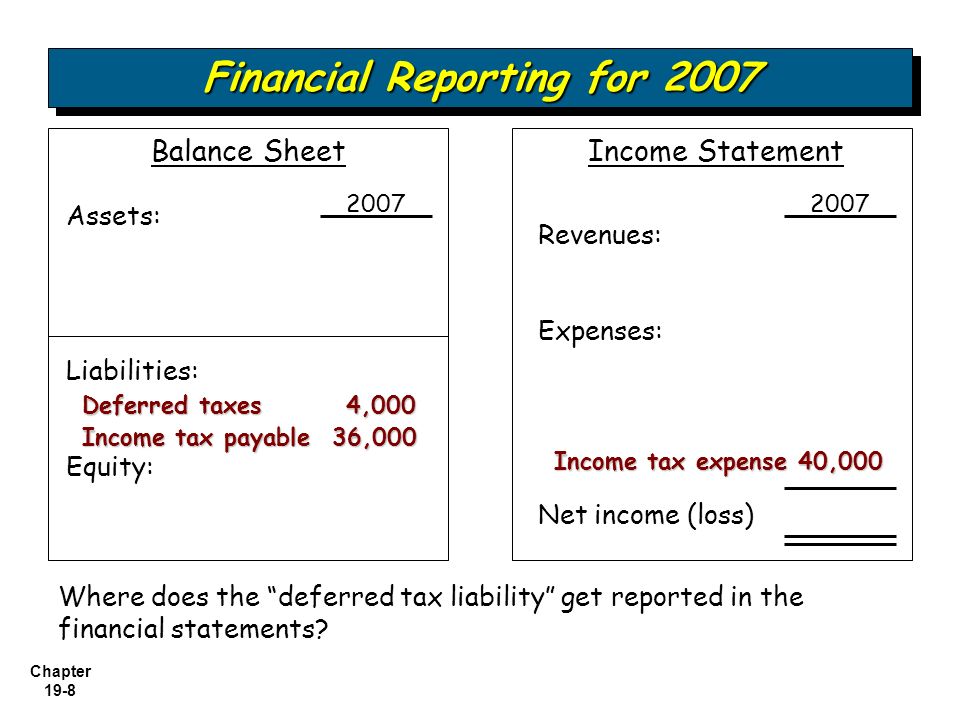

Chapter 19 1 Accounting For Income Taxes Chapter19 Intermediate Accounting 12th Edition Kieso Weygandt And Warfield Prepared By Coby Harmon University Ppt Download

DEFERRED TAX Deferred tax balance future tax payable or receivable on expected future transactions that have already been recognised in the financial statements as either assets or liabilities Deferred tax liability If assets future inflows liabilities future outflows expect future profit pay tax in future. The tax liability is calculated by adjusting the accounting income as per income tax laws. Definition Example And Calculation. One common cause of deferred tax liability is if a company uses accelerating depreciation for tax calculation and the straight-line method for accounting purpose. Follow these steps to calculate the deferred tax assetliability. 450000 then accounting profit will differ from IT profit. What is a Deferred Tax Liability. The title of the report is AASB 112 and analysis of financial statements. Deferred tax assets and liabilities are financial items on a companys balance sheet. Deferred tax assets and liabilities exist because the income on the tax return is different than income in the accounting records income per book.

The tax liability is calculated by adjusting the accounting income as per income tax laws.

Calculating a deferred tax balance the basics IAS 12 requires a mechanistic approach to the calculation of deferred tax. For example expenses that are amortized in the books over a period of time but allowed to be deducted completely in the first year. There can be other causes and you should know them well. A deferred tax is the difference between net income and income before taxes. 250000 and depreciation charged as per IT act is Rs. As the title suggests the main aim of the report is to understand the concept of the deferred tax assets and deferred tax liabilities.

Deferred tax liability can be defined as an income tax liability to the IRS for having tax payable less than what you actually incurred due to temporary differences between accounting income and taxable income. It is a line item booked under the. So to calculate income tax on this income the income is adjusted for various adjustments like disallowance of some expenses as per IT law. Definition Example And Calculation. Future tax consequences which give rise to deferred tax assets or deferred tax liabilities AASB 112 adopts a tax-effect method which is based on the assumption that the income tax expense in financial statements is not equal simply to the current tax liability but is also a function of the entitys deferred tax liabilities and deferred tax. Here are some transactions that generate deferred tax asset and liability balances. Notes to the consolidated financial statements 22 Appendices I New standards or amendments for 2016 and forthcoming requirements 150 II Presentation of comprehensive income Twostatement approach 152 III Statement of cash flows Direct method 154 IV Example disclosures for entities that early adopt Disclosure Initiative Amendments to. The tax liability is calculated by adjusting the accounting income as per income tax laws. What is a Deferred Tax Liability. Identify any assets and liability that have a different tax basis from its book value in the financial statements.

Follow these steps to calculate the deferred tax assetliability. The tax liability is calculated by adjusting the accounting income as per income tax laws. The sections of the guide are as follows. If depreciation charged for the year as per companies act is Rs. Deferred tax liability or deferred tax asset forms an important part of the year-end financial closure as it has an impact on the tax outflow of the company. For example expenses that are amortized in the books over a period of time but allowed to be deducted completely in the first year. The balance on the deferred tax liability account is 150 representing the future liability of the business to pay tax on the income for the period. For example income profit before tax of ABC Ltd. So to calculate income tax on this income the income is adjusted for various adjustments like disallowance of some expenses as per IT law. DEFERRED TAX Deferred tax balance future tax payable or receivable on expected future transactions that have already been recognised in the financial statements as either assets or liabilities Deferred tax liability If assets future inflows liabilities future outflows expect future profit pay tax in future.

Financial modeling deferred tax is an important step in the calculation of free cash flow Free Cash Flow FCF Free Cash Flow FCF measures a companys ability to produce what investors care most about. If depreciation charged for the year as per companies act is Rs. It is a line item booked under the. Identify any assets and liability that have a different tax basis from its book value in the financial statements. One of the key causes for preparing two statements to express similar financial events is the. For example if a company has an asset worth 10000 with a useful life of 10 years. In this article we will be discussing how to calculate deferred tax asset and liability that arises due to depreciation. Follow these steps to calculate the deferred tax assetliability. So to calculate income tax on this income the income is adjusted for various adjustments like disallowance of some expenses as per IT law. Any asset that has a higher book value is generally cause of a deferred tax.

The income tax payable account has a balance of 1850 representing the current tax payable to the tax authorities. The title of the report is AASB 112 and analysis of financial statements. Concept of Deferred Tax. What is a Deferred Tax Liability. Deferred tax assets and liabilities exist because the income on the tax return is different than income in the accounting records income per book. There can be other causes and you should know them well. Future tax consequences which give rise to deferred tax assets or deferred tax liabilities AASB 112 adopts a tax-effect method which is based on the assumption that the income tax expense in financial statements is not equal simply to the current tax liability but is also a function of the entitys deferred tax liabilities and deferred tax. The tax liability is calculated by adjusting the accounting income as per income tax laws. For example income profit before tax of ABC Ltd. Here are some transactions that generate deferred tax asset and liability balances.

Deferred Tax Liabilities Examples. One of the key causes for preparing two statements to express similar financial events is the. Follow these steps to calculate the deferred tax assetliability. For example if a company has an asset worth 10000 with a useful life of 10 years. Here are some transactions that generate deferred tax asset and liability balances. Future tax consequences which give rise to deferred tax assets or deferred tax liabilities AASB 112 adopts a tax-effect method which is based on the assumption that the income tax expense in financial statements is not equal simply to the current tax liability but is also a function of the entitys deferred tax liabilities and deferred tax. Calculating a deferred tax balance the basics IAS 12 requires a mechanistic approach to the calculation of deferred tax. One common cause of deferred tax liability is if a company uses accelerating depreciation for tax calculation and the straight-line method for accounting purpose. 450000 then accounting profit will differ from IT profit. In this article we will be discussing how to calculate deferred tax asset and liability that arises due to depreciation.