Variable Interest Entity Vie Definition Examples With Explanation

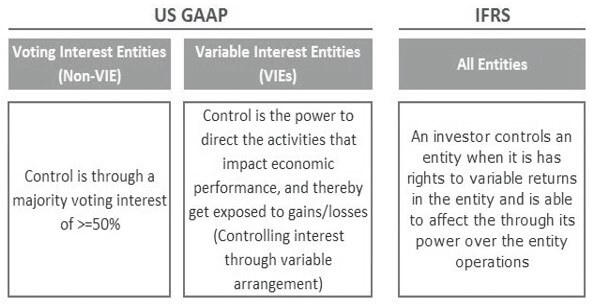

Under US GAAP all entities are first evaluated to determine whether they are variable interest entities VIEs. A VIE does not. A the power to direct the activities of the VIE that most significantly affect the VIEs economic performance and b the. 2111 Virtual SPEs or portions of legal entities. Under the VIE model a reporting entity has a controlling financial interest in a VIE if it has both. The voting interest model and The variable-interest entity VIE model. However for ease of reference we typically refer to public entities vs non-public entities with more nuanced discussion included in the appendix. GAAP that will let private companies skip the complex variable interest entity guidance in the consolidated reporting standard. 2121 VIE scope exception. What is a Variable Interest Entity.

For companies applying GAAP the consolidation guidance is included in ASC 810 Consolidationin particular the variable interest entity VIE subsections.

In order to apply the voting interest model however the VIE model must first be eliminated. The entitys equity is not sufficient to support its operations. US GAAP taxonomies up to 2019 included in the VIE section of the taxonomy a balance sheet location. What is a Variable Interest Entity. GAAP Amended to Give Private Companies Relief From VIE Guidance for Common Control Entities The FASB published an update to US. When an entitys voting equity interests control the entity then the VIE model does not apply.

For companies applying GAAP the consolidation guidance is included in ASC 810 Consolidationin particular the variable interest entity VIE subsections. For US GAAP requirements that are not yet fully effective this publication distinguishes the accounting. Consistent with historical practice business entities might look to IAS 20 as a source of. They are co-existing but mutually exclusive consolidation models. US GAAP taxonomies up to 2019 included in the VIE section of the taxonomy a balance sheet location. When an entitys voting equity interests control the entity then the VIE model does not apply. For other business entities US GAAP does not contain specific guidance on the accounting for government grants. 211 Consolidation background and general considerations. GAAP requires an organization including a private company to consolidate an entity in which it has a controlling financial interest. In order to apply the voting interest model however the VIE model must first be eliminated.

The VIE model was not intended to replace the voting interest model. If an entity is determined not to be a VIE it is assessed on the basis of voting and other decision-making rights under the voting interest model. A VIE is a authorized construction the place the occasion with the controlling curiosity doesnt essentially have nearly all of the voting rights. Unlike IFRS US GAAP has specialized industry accounting requirements for not-for-profit entities NFPs that receive government grants. 21 Scope of consolidation guidance. Under the VIE model a reporting entity has a controlling financial interest in a VIE if it has both. For other business entities US GAAP does not contain specific guidance on the accounting for government grants. The definition of a VIE in ASC 810-10-20 is not helpful at all A legal entity subject to consolidation according to the provisions of the Variable Interest Entities Subsection of Subtopic 810-10. Consistent with historical practice business entities might look to IAS 20 as a source of. Under US GAAP all entities are first evaluated to determine whether they are variable interest entities VIEs.

Consistent with historical practice business entities might look to IAS 20 as a source of. However for ease of reference we typically refer to public entities vs non-public entities with more nuanced discussion included in the appendix. The entitys equity is not sufficient to support its operations. 2111 Virtual SPEs or portions of legal entities. The VIE model was not intended to replace the voting interest model. US GAAP taxonomies up to 2019 included in the VIE section of the taxonomy a balance sheet location. Unlike IFRS US GAAP has specialized industry accounting requirements for not-for-profit entities NFPs that receive government grants. GAAP that will let private companies skip the complex variable interest entity guidance in the consolidated reporting standard. When an entitys voting equity interests control the entity then the VIE model does not apply. 511 Application of VIE Guidance to Multitiered Legal-Entity Structures 131 512 Anticipating Changes in the Design of a Legal Entity 131 52 Sufficiency of Equity 132 521 Identifying Whether an Interest in a Legal Entity Is Considered GAAP Equity Step 1 133.

The VIE model was not intended to replace the voting interest model. 211 Consolidation background and general considerations. If the voting mannequin was used for consolidation in these instances the controlling occasion or main beneficiary wouldnt be required to consolidate the subsidiary which leads to deceptive consolidated monetary statements. 2111 Virtual SPEs or portions of legal entities. 21 Scope of consolidation guidance. Unlike IFRS US GAAP has specialized industry accounting requirements for not-for-profit entities NFPs that receive government grants. If an entity is determined not to be a VIE it is assessed on the basis of voting and other decision-making rights under the voting interest model. If the VIE model is not applicable then entities are subjected to the voting interest model. Under the VIE model a reporting entity has a controlling financial interest in a VIE if it has both. A VIE is a authorized construction the place the occasion with the controlling curiosity doesnt essentially have nearly all of the voting rights.

Unlike IFRS US GAAP has specialized industry accounting requirements for not-for-profit entities NFPs that receive government grants. What is a Variable Interest Entity. The VIE model was not intended to replace the voting interest model. There are two primary models for assessing whether an entity has a controlling financial interest in another entity. For other business entities US GAAP does not contain specific guidance on the accounting for government grants. If an entity is determined not to be a VIE it is assessed on the basis of voting and other decision-making rights under the voting interest model. Under US GAAP all entities are first evaluated to determine whether they are variable interest entities VIEs. 2112 Consolidation of majority-owned or wholly-owned subsidiaries. GAAP Amended to Give Private Companies Relief From VIE Guidance for Common Control Entities The FASB published an update to US. Consistent with historical practice business entities might look to IAS 20 as a source of.