Unique Use The Following Information To Prepare A Trial Balance Audit Fees In Sheet

Prepare Financial Statements Using The Adjusted Trial Balance Principles Of Accounting Volume 1 Financial Accounting

Using the following information prepare a trial balance. Assume all asset dividend and expense accounts have debit balances and all liability stockholders equity and revenue accounts have credit balances. Equipment was recently purchased so there is neither depreciation expense nor accumulated depreciation. The purpose of a trial balance is to ensure that all entries made into an organizations general ledger are properly balanced. Dividends assume accounts have normal balances. The total dollar amount of the debits and credits in each accounting entry are supposed to match. Assets Liabilities Equity Dividends Revenues and Expenses. Assets liabilities stockholders equity dividends revenues and expenses. Using the following information prepare a trial balance. So firstly every ledger account must be balanced.

Adjusting entries are added in the next column yielding an adjusted trial balance in the far right column.

1 Mira prepared a trial balance using the following information on 31 March 2015. The most important difference is that a balance sheet is a financial statement that is used to report a companys liabilities assets and stockholders equity at a particular date. Assets liabilities stockholders equity dividends revenues and expenses. The total dollar amount of the debits and credits in each accounting entry are supposed to match. Using the following information prepare a trial balance. List the accounts in the following order.

Solve for the one missing account balance. This trial balance is an important step in the accounting process because it helps identify any computational errors throughout the first five steps in the cycle. The purpose of a trial balance is to ensure that all entries made into an organizations general ledger are properly balanced. Trial balance of Tyndall at 31 May 20X6. A Nov 1 Reimbursed Grahams business automobile expense for 1000 kilometers at 100 per kilometer. Some important distinctions here must be made between a trial balance vs balance sheet. A trial balance lists the ending balance in each general ledger account. In this totals method we ascertain the total of each side in the ledger ie. This is done to determine that debits equal credits in the recording process. To prepare a trial balance you need to list the ledger accounts along with their respective debit or credit amounts.

Accounting questions and answers. Using the following information prepare a trial balance. Some important distinctions here must be made between a trial balance vs balance sheet. Preparing the trial balance perfectly ensures that the final accounts are error-free. In this totals method we ascertain the total of each side in the ledger ie. 1 Closing inventory has been valued for accounts purposes at 8490. Adjusting entries are added in the next column yielding an adjusted trial balance in the far right column. From this information the company will begin constructing each of the statements beginning with the income statement. Cash 6200 Dividends 1200 Deferred. A trial balance lists the ending balance in each general ledger account.

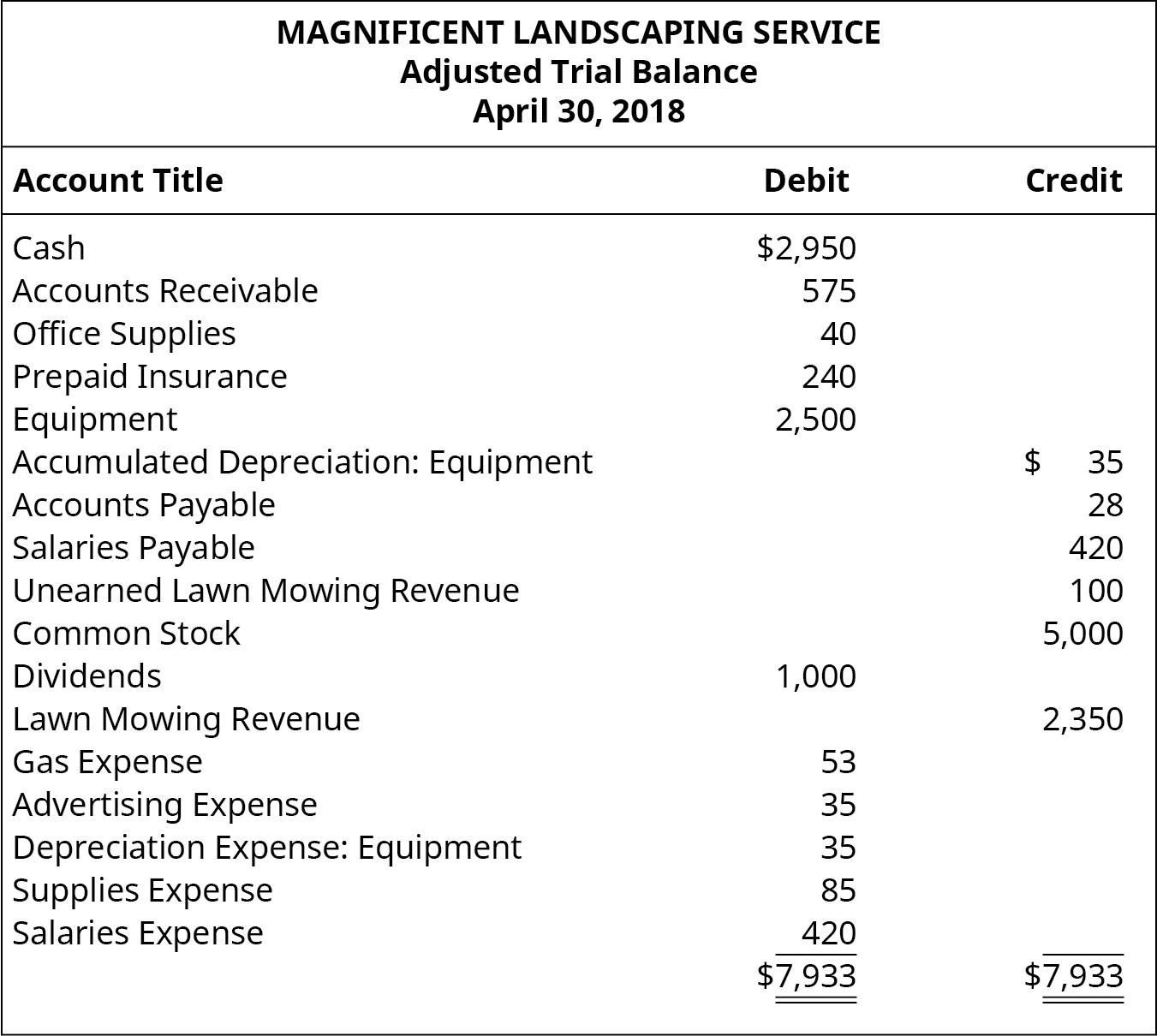

We can prepare the Trial Balance in the following three ways. Assume all asset dividend and expense accounts have debit balances and all liability stockholders equity and revenue accounts have credit balances. To prepare the financial statements a company will look at the adjusted trial balance for account information. The trial balance information for Printing Plus is shown previously. Income statement s will. Preparing the trial balance perfectly ensures that the final accounts are error-free. Preparing and adjusting trial balances aid in. Cash 6200 Dividends 1200 Deferred Revenue 1200 Salaries Expense 2200 Prepaid Insurance 1200 Accounts Receivable 3400 Accounts Payable. Accountants use a trial balance to test the equality of their debits and credits. This is done to determine that debits equal credits in the recording process.

Equipment was recently purchased so there is neither depreciation expense nor accumulated depreciation. In this example we will account for the period-end adjustments and prepare a set of financial statements from a TB. Using the following information prepare a trial balance. The trial balance information for Printing Plus is shown previously. This trial balance is an important step in the accounting process because it helps identify any computational errors throughout the first five steps in the cycle. Adjusting entries are added in the next column yielding an adjusted trial balance in the far right column. Some important distinctions here must be made between a trial balance vs balance sheet. To prepare a trial balance you need to list the ledger accounts along with their respective debit or credit amounts. Balancing is the difference between the sum of all the debit entries and the sum of all the credit entries. Assume all asset dividend and expense accounts have debit balances and all liability stockholders equity and revenue accounts have credit balances.

From this information the company will begin constructing each of the statements beginning with the income statement. Use the following information to prepare a trial balance. Accountants use a trial balance to test the equality of their debits and credits. 1 Mira prepared a trial balance using the following information on 31 March 2015. Assets liabilities stockholders equity dividends revenues and expenses. The total dollar amount of the debits and credits in each accounting entry are supposed to match. The information from the trial balance is used to prepare the balance sheet. The purpose of a trial balance is to ensure that all entries made into an organizations general ledger are properly balanced. To prepare a trial balance we need the closing balances of all the ledger accounts and the cash book as well as the bank book. After a company posts its day-to-day journal entries it can begin transferring that information to the trial balance columns of the 10-column worksheet.